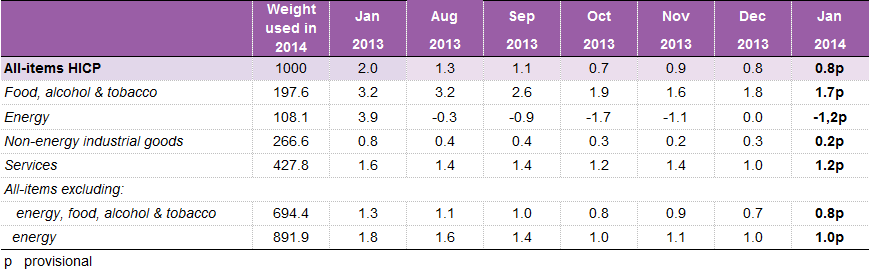

Eurostat table: Euro area annual inflation and its main components (%).

Harmonised indices of consumer prices (HICP)

Eurostat graph: Weights of the main components of the euro area harmonised indices of consumer prices (HICP)

Share this Sting:

Discover more from The European Sting - Critical News & Insights on European Politics, Economy, Foreign Affairs, Business & Technology - europeansting.com

Subscribe to get the latest posts sent to your email.

Why don't you drop your comment here?